Louisiana’s “No-Pay, No-Play” Law (and 5 Exceptions)

(Last Updated: November 19, 2025)

Louisiana’s “No Pay, No Play” law prevents uninsured (and under-insured) drivers that have been involved in an auto accident from recovering bodily injury damages up to the first $100,000, and property damages (vehicle damages) up to the first $100,000.

However, there are five exceptions to the Louisiana No Pay, No Play law →

What is Louisiana’s “No Pay, No Play” Law?

Exceptions to Louisiana’s “No-Pay, No Play” Law? →

Louisiana’s No Pay, No Play Statute →

What if the At-Fault Driver Did Not Have Auto Accident Insurance? →

Uninsured Drivers in Louisiana →

Arguments For and Against No Pay, No Play →

No Pay, No Play Laws Nationally →

IMPORTANT – PLEASE NOTE: If you have been involved in an auto accident in Louisiana and suffered only property damage, minor injuries, or no injuries at all, and did not have car insurance at the time of the wreck, our New Orleans car accident lawyer will be unable to help you pursue a claim unless you qualify for one of the “No-Pay, No-Play” law’s exceptions (see below).

What is Louisiana’s “No Pay, No Play” Law?

In Louisiana, the “No-Pay, No Play” law prevents uninsured and under-insured drivers from collecting the first $100,000 of bodily injury damages and the first $100,000 of property damages. This means that even if the other driver is at fault, an uninsured driver will have to cover medical costs up to $100,000, and car damage repairs up to $100,000.

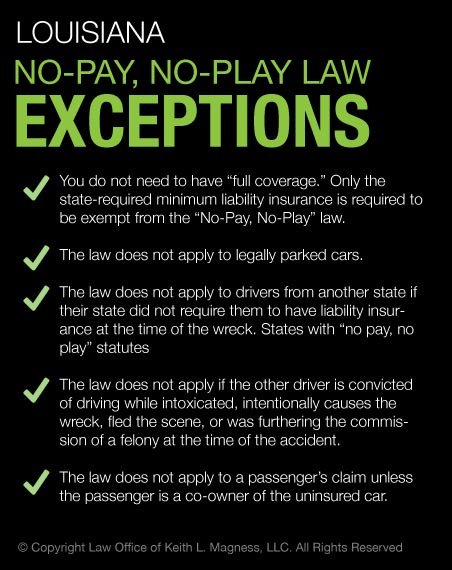

Are There Exceptions to the Louisiana “No-Pay, No-Play” Law?

Yes. If you’ve been injured in a car accident, Louisiana’s “No Pay, No Play” law has multiple exceptions you should be aware of:

- You do not need to have “full coverage.” Only the state-required minimum liability insurance is required to be exempt from the “No-Pay, No-Play” law.

- The law does not apply to legally parked cars.

- The law does not apply to drivers from another state if their state did not require them to have liability insurance at the time of the wreck. States with “no pay, no play” statutes »

- The law does not apply if the other driver is convicted of driving while intoxicated, intentionally causes the wreck, fled the scene, or was furthering the commission of a felony at the time of the accident.

- The law does not apply to a passenger’s claim unless the passenger is a co-owner of the uninsured car.

If you believe you qualify for one of the exceptions to the Louisiana No-Pay, No Play law, be sure to contact an experienced auto accident injury lawyer to review your case; and be sure to avoid common mistakes following a car accident in New Orleans that can harm your claim. Additionally, review what to do after you’ve been in a car accident, so you can avoid costly mistakes.

Louisiana’s “No Pay, No Play” Statute (La. R.S. § 32:866), Amended in 2025

The statute which passed in 2011 and was amended in 2025, reads in part:

“There shall be no recovery for the first one hundred thousand dollars of bodily injury and no recovery for the first one hundred thousand dollars of property damage based on any cause or right of action arising out of a motor vehicle accident, for such injury or damages occasioned by an owner or operator of a motor vehicle involved in such accident who fails to own or maintain compulsory motor vehicle liability security.”

Client Testimonial

“I was hesitant to speak with an attorney because of my “No Pay, No Play” situation. I needed help fixing my car. Keith went above and beyond to satisfy my claim. Keith kept his word, and his staff was very friendly, caring and treated me as family. I’m so happy I chose [Keith and his team] and will refer [them] to everyone.”

– Dana (from Harvey, Louisiana)

Read more New Orleans car accident lawyer reviews here »

What If the At-Fault Driver Does Not Have Auto Accident Insurance?

Normally, the insurance company of the person who is at fault for an auto accident is responsible for paying the cost of repairs to the driver who was not at fault. If the at-fault driver does not have insurance, these costs may go unpaid. In most cases, when a person files a claim his or her insurance company pursues the other party’s carrier through a process called subrogation. But if the at-fault driver does not have insurance, the insurance company must try to collect funds directly from the driver. If this is unsuccessful – and it often is – the insurance company has to increase the premiums for its customers in order to off-set the lost money spent on claims.

Uninsured Drivers in Louisiana

Louisiana is the second most expensive state for auto insurance – partly because of its high number of uninsured drivers. In an effort to reduce insurance premiums for its consumers, among other initiatives, the state legislature passed Act 1476, known as the Omnibus Premium Reduction Act, in 1997. One section of this complex law was the “No-Pay, No-Play” provision, enacted to penalize uninsured and underinsured drivers, while encouraging them to purchase adequate levels of insurance.

Arguments For And Against the No Pay, No Play Statute in Louisiana

Opponents of No-Pay, No-Play contend that the reason that uninsured drivers don’t have insurance is because they can’t afford it, and the law simply punishes people who are already in a difficult financial situation.

However, proponents of the law believe it is necessary, in the name of fairness: uninsured drivers shouldn’t be rewarded by a system they have neglected to pay into. Nor should they be able to benefit from law-abiding drivers’ insurance, while denying that same privilege to any drivers they themselves happen to hit.

No Pay, No Play Laws Nationally

According to the Insurance Research Council (IRC), roughly 14 percent of all motorists in the U.S. are uninsured – that’s nearly one out of every seven drivers. States with a high number of uninsured drivers also tend to have higher insurance costs. That is because accidents caused by uninsured drivers cause insurance companies to lose money.

States with No Pay, No Play Laws

Several states have adopted some version of “no pay, no play” laws to discourage drivers from not insuring their vehicles. These laws limit the damages an uninsured driver can recover after a crash, based on the principle that those who don’t contribute to the insurance system should not be eligible to receive full benefits from it.

| State | Restriction (e.g. “No Pay, No Play”) | Statute |

| Alaska | Uninsured drivers cannot recover non-economic damages (e.g. pain and suffering) for injuries or death suffered while driving uninsured, unless the at-fault driver was under the influence, acted intentionally or recklessly, or fled the scene. | Alaska Stat. § 09.65.320 |

| California | A driver who is uninsured (or driving under the influence, or unable to prove financial responsibility) cannot recover non-economic damages after an accident, unless the at-fault driver was also under the influence and convicted of that offense. | Cal. Civ. Code § 3333.4 |

| Indiana | An uninsured driver with a prior uninsured-driving violation (within the past five years) forfeits the right to recover non-economic damages from an at-fault motorist . | Ind. Code §§ 27-7-5.1; 34-30-29.2 |

| Iowa | If an injured driver was in the act of committing a felony during the accident and is convicted of that felony, they are barred from recovering non-economic damages. | Iowa Code § 613.20 |

| Kansas | A driver who fails to maintain the required personal injury protection insurance (or any uninsured driver) has no cause of action for non-economic losses after an accident, and likewise a DUI-convicted driver is barred from non-economic damages . | Kan. Stat. Ann. § 40-3130 |

| Louisiana | For accidents on or after August 1, 2025, an uninsured driver cannot recover the first $100,000 of bodily injury damages and the first $100,000 of property damage, subject to the usual exceptions (e.g., at-fault driver is DWI, intentional act, hit-and-run, certain felony conduct, etc.), under La. R.S. 32:866 as amended by HB 434 / Act 16 (2025). | La. Rev. Stat. § 32:866 |

| Michigan | An uninsured motorist injured in a crash is barred from recovering any damages if they did not carry the mandatory auto liability insurance at the time of the accident. | Mich. Comp. Laws § 500.3135(2)(c) |

| Missouri | An uninsured motorist waives the right to sue for any damages against an at-fault driver if uninsured at the time of the accident, unless the at-fault driver was under the influence during the accident. | Mo. Rev. Stat. § 303.390 |

| New Jersey | Uninsured drivers (as well as drivers under the influence or acting with intent to harm themselves or others) are barred from recovering both economic and non-economic damages after an accident. | N.J. Stat. Ann. § 39:6A-4.5 |

| North Dakota | An uninsured driver with at least one prior conviction for driving without insurance cannot recover non-economic damages from an insured at-fault driver in an accident. | N.D. Cent. Code § 26.1-41-20 |

| Oregon | An uninsured plaintiff may not recover non-economic damages from an insured at-fault party, unless the at-fault driver was acting intentionally, recklessly, or was committing a felony at the time of the accident. | Or. Rev. Stat. § 31.715 |

Unlike Louisiana many states with No-pay, No-play limitations on car insurance claims (and lawsuits) are only on non-economic damages. This would include items such as pain and suffering, mental anguish, and loss of companionship. Economic damages, the uninsured motorist’s actual medical bills, and property damage, are typically still recoverable in these jurisdictions.

Louisiana is the only state whose law specifically enumerates “No-pay, No-play deductible amounts,” which are equal to the state-required minimum bodily injury and property damage liability coverages for motorists.

For questions about a car accident in the New Orleans area, contact the experienced team at the Law Office of Keith L. Magness, LLC today at (504) 264-5587.